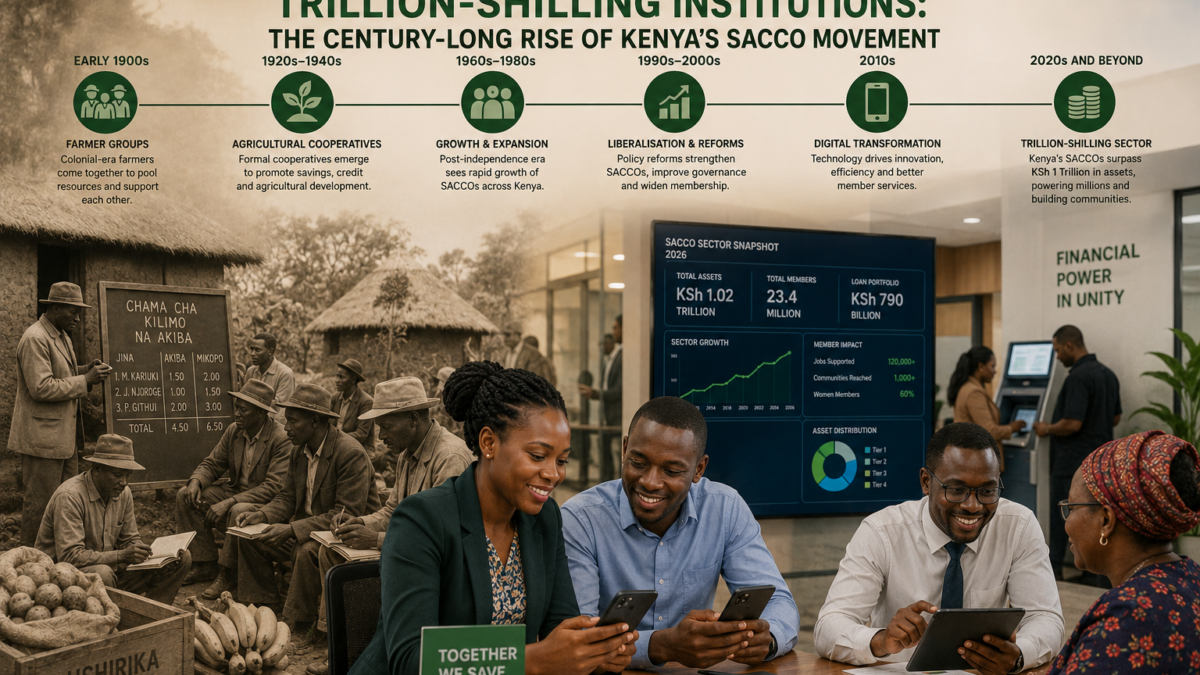

Long before Kenya’s savings and credit cooperatives became the trillion-shilling financial force they are today, the movement’s roots lay in small farmer associations formed in the central highlands and Rift Valley during the colonial era, when groups of growers pooled savings and bargaining power to escape dependence on moneylenders and middlemen controlling access to markets and credit.

Some of the earliest cooperative structures in the country date to the 1920s, when organizations such as the Kenya Planters’ Co-operative Union and, somewhat later, the Kenya Co-operative Creameries were established to help farmers market coffee and dairy products collectively while gaining access to affordable financing for inputs and equipment. Smaller, localized savings groups, including early farmer cooperatives in areas such as the Lumbwa Valley, laid further groundwork for what would eventually become a nationwide movement built specifically around savings and credit, as distinct from marketing cooperatives focused on a single crop or product.

The concept of a dedicated savings and credit cooperative, pooling members’ deposits specifically to provide credit facilities to fellow members, traces its global lineage to 19th-century rural Europe, where cooperative pioneers developed the model as an alternative to dependence on merchants and moneylenders for agricultural financing. The approach reached Africa in the 1950s, with one of the continent’s earliest documented savings and credit cooperatives established in Ghana in 1955 by a Catholic missionary who had studied the model in Canada. From there, the concept spread across the continent over the following decade, arriving in Kenya as the country approached independence.

Kenya’s cooperative movement expanded rapidly after independence in 1963, as the new government actively encouraged cooperative formation as a tool for national development and financial inclusion, particularly in rural areas where formal banking infrastructure remained thin. That policy push was formalized in 1968 with the enactment of the Cooperative Societies Act, which established the first comprehensive legal framework governing how cooperatives, including savings and credit societies, could register and operate in Kenya. The legislation triggered a wave of new cooperative formation through the 1970s, as the model that had begun with agricultural marketing cooperatives extended into a distinct category built specifically around member savings and credit.

That decade produced many of the occupation-based SACCOs that remain among the sector’s largest institutions today. Kenya National Police Sacco traces its origins to 1972, when it began with just 690 members drawn from the police service. Mwalimu National Sacco, now Kenya’s largest cooperative by asset base, was founded in 1974 by a group of primary school teachers in Ol’Kalou with just nine founding members, growing over the following five decades into an institution serving well over 100,000 members nationwide. Stima Sacco was also established in 1974, initially to serve employees of the former East African Power and Lighting Company, the predecessor to today’s Kenya Power, before broadening its membership over time to include corporations, groups and individual business owners well beyond the electricity sector. Harambee Sacco, catering to civil servants, and a wide range of teacher-focused cooperatives in specific regions, including Gusii Mwalimu Sacco in 1979 and Mentor Sacco (originally the Murang’a District Teachers Cooperative Society) in 1977, followed a similar pattern of professional groups organizing their own savings and credit institutions around a shared employer or payroll system.

As the number of individual SACCOs multiplied, the movement recognized the need for a coordinating national body. In 1972, a national promotion committee studied how best to structure an umbrella association capable of representing SACCOs collectively, leading to the registration of the Kenya Union of Savings and Credit Co-operatives, known as KUSCCO, on September 27, 1973, with operations beginning the following year. KUSCCO has since functioned as the principal national organization for the movement, offering advocacy, risk management services, a central finance facility, training and a housing fund for affiliated SACCOs, and describes the Kenyan SACCO movement as the largest in Africa and among the ten largest cooperative savings and credit systems in the world. Kenya’s cooperative sector also built early international ties through the World Council of Credit Unions, which worked with the Kenyan movement on agricultural development, technology and financial inclusion programs beginning in 1980 and continuing, with some interruption, through 2017.

For much of this history, SACCOs operated under a comparatively light regulatory touch, supervised primarily through the Ministry of Cooperative Development rather than a dedicated financial sector regulator. That changed with the Sacco Societies Act of 2008, which established the Sacco Societies Regulatory Authority, or SASRA, and introduced bank-style prudential supervision, including capital adequacy and liquidity requirements, specifically for deposit-taking SACCOs. The reform reflected growing recognition that cooperatives holding substantial member deposits and offering over-the-counter banking-style services needed a supervisory framework closer to that applied to commercial banks, rather than the lighter administrative oversight historically applied to cooperatives more broadly. Non-deposit-taking societies, which remain far more numerous but individually far smaller, continued to fall under the Commissioner for Cooperatives, entrenching the two-tier supervisory structure that still characterizes the sector today.

Individual SACCOs have periodically claimed a series of sector firsts along the way, each marking a small step in the movement’s gradual modernization. Stima Sacco, for instance, describes itself as the first Kenyan SACCO to be licensed by SASRA after the 2008 reforms, the first to introduce mobile banking services to its members, the first to launch ATM access, and the first to roll out Sharia-compliant financial products alongside its conventional savings and credit offerings. More recently, in November 2025, Stima became the first SACCO to connect fully to Pesalink, Kenya’s instant interbank payment network, a milestone industry figures frame as a continuation of the same pattern of incremental modernization that has defined individual SACCOs’ competitive positioning within the wider movement for decades. Other large cooperatives have pursued comparable firsts in areas such as bancassurance, welfare and last-expense benefit schemes, and diaspora membership products aimed at the substantial number of Kenyans living and working abroad who continue to maintain savings and family ties at home.

The movement’s international connections have also deepened in recent years, extending beyond the long-standing relationship with the World Council of Credit Unions. In 2025, the African Confederation of Cooperative Savings and Credit Associations and the global payments company Visa announced a partnership aimed at expanding access to formal financial services across Kenya and neighboring Tanzania by leveraging existing cooperative and SACCO infrastructure alongside Visa’s payments network, part of a broader pattern of international payment and technology providers viewing Africa’s cooperative sector as an underused channel for extending formal financial services to unbanked and underbanked populations. Cooperative leaders have also periodically explored how SACCOs might complement state-backed lending initiatives aimed at youth and informal-sector workers, arguing that the sector’s combination of savings discipline and member ownership offers a more sustainable complement to purely credit-focused government programs than stand-alone lending schemes alone.

The results of that regulatory evolution, combined with sustained membership growth, have been substantial. Sector assets held by SASRA-regulated SACCOs have more than tripled over the past decade, rising from roughly 301.54 billion shillings in 2014 to surpass 1 trillion shillings for the first time by the end of 2024, according to the regulator’s most recent supervision report. Membership across regulated SACCOs has more than doubled over the same period, from about 3.08 million people to more than 7.39 million, while total deposits mobilized from members have nearly quadrupled, growing from roughly 205.97 billion shillings to 749.43 billion shillings. SASRA notes that the sector’s assets now represent about 6.63% of Kenya’s nominal gross domestic product, up from 5.59% a decade earlier, and that Kenya’s credit union system ranks 14th globally by total assets, a scale unmatched elsewhere on the continent.

That growth has not been without setbacks that echo the governance challenges the movement has wrestled with since its earliest decades. KUSCCO itself, the umbrella body founded in 1973, was placed under an interim board in 2024 following allegations of fraud and mismanagement connected to member funds channeled through its investment arm, an episode that prompted the Cabinet Secretary for Cooperatives and MSMEs Development to personally inaugurate a new interim leadership team and press for stronger transparency and accountability commitments across the union’s affiliated societies. Some individual SACCOs disclosed significant exposure to KUSCCO-linked investment vehicles as the crisis unfolded, prompting fresh scrutiny of how much of members’ life savings had been placed in less transparent, KUSCCO-administered instruments rather than each SACCO’s own regulated balance sheet. Officials have since described fraud, mismanagement and gaps in legislative oversight as recurring challenges for the cooperative movement, even as they credit SACCOs broadly with expanding the reach of affordable savings and credit services to households at the lower end of Kenya’s income distribution who might otherwise depend on informal lenders.

That tension between celebrating the movement’s scale and confronting its governance gaps runs through Kenya’s cooperative sector today much as it did in earlier decades, when isolated cases of mismanagement periodically tested confidence in individual SACCOs even as the broader movement continued to expand. The government’s current push to deregister thousands of non-compliant cooperatives, alongside proposed amendments to the Sacco Societies Act and a new deposit protection framework, represents the latest chapter in a decades-long pattern of the sector outgrowing its existing oversight architecture and then working, often under public pressure, to catch up.

For the millions of Kenyans who now belong to a SACCO, whether through a teachers’ cooperative with roots stretching back fifty years or a newly formed community-based society registered only in the past few years, the movement’s history offers a particular kind of reassurance and caution in equal measure: reassurance, in that SACCOs have proven a durable and adaptable institution capable of scaling from a handful of colonial-era farmer groups to a trillion-shilling pillar of the national financial system; and caution, in that the same decentralized, member-driven structure that has allowed the movement to grow so widely has also, at multiple points across a century, made consistent governance and oversight one of its most persistent unresolved challenges.

Marking KUSCCO’s fiftieth anniversary in 2023, government officials used the occasion to simultaneously celebrate the movement’s longevity and warn publicly about the risk of fraud within cooperative societies, a pairing that captures how Kenya’s SACCO story has rarely allowed one theme to be told without the other. Half a century after nine teachers in Ol’Kalou pooled their savings to found what would become the country’s largest cooperative, and more than a century after the earliest farmer associations organized in the central highlands, the movement’s next chapter looks set to be written at the intersection of the same two forces that have shaped it from the beginning: the steady expansion of member savings and credit into new communities and professions, and the recurring challenge of ensuring governance keeps pace with that growth.

(Reporting compiled from historical accounts published by the Kenya Union of Savings and Credit Co-operatives (KUSCCO), the World Council of Credit Unions, cooperative sector publications including Sacco Review, and supervision data published by the Sacco Societies Regulatory Authority (SASRA).)

This content is provided for general informational and news purposes only and does not constitute financial or investment advice. Readers should verify current SACCO information directly with SASRA or the relevant institution and consult a qualified financial adviser before making savings or investment decisions.